Wallet Report v2

Dive into the data behind the evolution of wallets, from MetaMask and Phantom to Coinbase and Safe, in our latest deep-dive on embedded swap activity, smart accounts, and the rise of wallet infrastructure.

Exclusive content

Download Content

Editor’s Note

Wallets are arguably the most widely used product in crypto. Whether explicitly or not, they are the gateway to nearly every onchain interaction, including swapping tokens, minting NFTs, and participating in governance. Yet despite their central role, wallets remain surprisingly underexplored in data-driven research.

Part of the challenge is that “wallet” isn’t a single category—it spans custodial and non-custodial models, EOAs and smart accounts, mobile apps and backend SDKs. Custodial wallets leave little onchain data, while non-custodial ones generate traceable signals, although these are fragmented across architectures (EOA, smart contract, EIP-7702 hybrids), standards (account abstraction has ERC-4337, Safe’s modular approach, Argent early adoption, etc), and tooling layers. Today’s wallet systems are often modular: Coinbase Smart Wallets may be deployed via apps like Zora with Privy managing access; Layer3 new wallet uses a smart account architecture built on abstraction layers like ZeroDev Kernel, Pimlico, Turnkey and Dune Echo; and tools like Privy or Reown’s AppKit abstract wallet logic entirely. The boundary between frontend, backend, and wallet is increasingly blurred.

Therefore, rather than presenting a single unified narrative, this report is structured as an anthology of the wallet ecosystem. We explore the space through a series of standalone but complementary sections, each grounded in distinct dashboards, datasets, and methodologies. This format reflects the true nature of wallets today: diverse, fast-moving, and shaped by parallel innovations.

To continue improving this picture, we invite wallet providers, analysts, and researchers to reach out and share additional data, insights, and context. By working together, we can build the most accurate and nuanced map of wallet usage across crypto.

🅽🅴🆆 What’s new in Version 2?

This edition introduces improved datasets and a refined methodology for analyzing embedded swap activity from EOAs. We expand coverage with updated data on Phantom’s newest features, and add dedicated sections on Uniswap Wallet and Meteor in the EOA category. The smart wallet section now includes Biconomy’s evolving stack and Abstract Global Wallet’s chain-native architecture. We also present early adoption metrics for EIP-7702 in its first month live, and introduce Dynamic as a key player powering hybrid wallet infrastructure.

If you have read the V1 report, you can navigate through the table of contents for all the newly added sections.

Key Insights

- Wallet activity is surging: From embedded swap transfers to UserOperations, nearly every metric points to rising onchain engagement through wallets. Whether via embedded DEX routers or smart account interactions, wallets are no longer passive interfaces; they’re where much of crypto’s daily activity happens.

- Wallet adoption is geographically diversifying: Emerging markets are driving a growing share of wallet activity, with countries like Nigeria, India, Vietnam, and Indonesia consistently ranking among the top user bases across many wallets analyzed. This trend highlights wallets' expanding role as financial access points in regions underserved by traditional infrastructure.

- UX is converging toward seamlessness: Passkeys, gas sponsorship, and chain abstraction are becoming baseline. This reflects an industry-wide push to reduce friction and make complex interactions feel familiar, signaling a maturation in smart wallet design and implementation.

- Wallets are becoming self-contained superapps: The clearest trend is vertical expansion where wallets now embed swaps, staking, quests, bridging, and even game discovery. Rather than simply storing assets, they connect, curate, route, and increasingly own the user journey, blurring the line between tool and platform.

- Infrastructure is becoming more modular: Solutions like Privy, Reown and Dynamic show how wallet functionality is being abstracted into plug-and-play infrastructure—provisioned at login, embedded into apps, and invisible to end users. This shift enables apps to deliver wallet-powered experiences without exposing the underlying mechanics.

- Dune’s role in supporting wallet development: Data, whether used as analytics or realtime for backend development, is the key to wallet innovation. Dune is looking to expand its role in making the wallet landscape more vibrant with additional developer solutions on realtime wallet data APIs.

Introduction to Crypto Wallets

Crypto wallets are the primary interface for interacting with blockchain networks. They allow users to store and manage digital assets (like cryptocurrencies, NFTs, and tokenized assets), authorize transactions, and access onchain applications. Wallets don’t store assets directly—instead, they secure the private keys that prove ownership and enable transactions.

Hardware vs. Software

- Hardware wallets (e.g., Ledger, Trezor) store keys offline for enhanced security but require physical interaction.

- Software wallets (e.g., MetaMask) are mobile, desktop, or browser-based, easier to use but more exposed to online risks.

Custodial vs. Non-Custodial

- Custodial wallets (e.g., Binance, Coinbase) are managed by third parties who control users' keys, simplifying access but requiring trust.

- Non-custodial wallets give users full control over their keys and funds, aligned with crypto’s ethos but shifting security responsibility to the user. Almost all centralized exchanges offer a self-custodial wallet besides the default custodial one.

Security Models: MPC and Multisig

- MPC (Multi-Party Cobimputation) splits a key across multiple devices or servers to avoid single-point exposure.

- Multisig requires multiple private key signatures to approve a transaction, common in DAOs and treasuries.

Smart Contract Wallets and Recovery

Smart contract wallets (or smart accounts) replace private keys with smart contracts. A key feature enabled is social recovery, allowing users to regain access via trusted guardians or devices. This blends the convenience of custodial models with the security and control of non-custodial systems.

Section 01 - EOA Wallets

“MetaMask remains the bridge for millions entering Web3—offering global access while adapting to evolving user needs.”

– MetaMask Team

“Bitget Wallet reflects the growing demand for high-speed, mobile-first trading experiences in Web3—where swaps, staking, and dApps converge in a single interface designed to make crypto simple for everyone.”

– Alvin Kan, COO of Bitget Wallet

Measuring Embedded Swap Activity

Dashboard: Wallet Overview

Data credits: mausefalle and 0xpibs for building the dataset and the main queries. Shoutout also to lz_web3 for creating the dashboard that served as inspiration for this analysis.

One way to analyze onchain wallet usage for externally owned account (EOA) wallets is to track the activity of their embedded swap functions. For this section, we mapped known router contract addresses used by wallets like MetaMask, Trust Wallet, Bitget, and others to power their in-app swaps. Using the tokens.transfers table on Dune, we queried transfer counts and transfer volumes to these swap router addresses. This provides a proxy for swap usage originating directly from within EOA wallet interfaces.

🅽🅴🆆 V2: Improved dataset and methodology

In this v2, we introduce an improved dataset and methodology to enhance accuracy and transparency. Key updates include:

- Address Filtering: We removed mislabeled or ambiguous addresses and added newly verified router addresses for OKX.

- Deduplication: In the transfer event subquery, we now deduplicate multiple “to” = routerAddress transfer events occurring within the same transaction hash. This ensures we count only one event per transaction to prevent inflated swap counts or volumes.

- Chain-Specific Address Matching: Rather than treating a router address as universal across chains, we now match each address with the corresponding blockchain/s where the address could be verified. This allows for greater precision in attribution. As a result, we've introduced a new category, ‘Unknown’, which includes address-chain pairs we couldn’t confidently verify. These may reflect either unlabeled but valid router addresses, or unrelated contracts altogether.

Measuring In-Wallet Swap Activity

To summarize, our methodology consists of a main query made of two complementary subqueries:

- Transfer Event Analysis (“to” = routerAddress). Captures explicit token transfers from users to router addresses, reflecting the input side of a swap.

- Transaction-Level Analysis (tx_to = routerAddress). Captures swaps where no direct “to” = router event exists. Here, we select transfers where the transaction’s tx_to is the router, “tx_from” is the user but “to” is not the router, to avoid overlapping with the previous query.

For Rabby and Coinbase Wallet, which don’t use routers, we track their known fee-collecting EOAs and back-calculate the swap volume based on fees collected.

Limitations

- Tron, Bitcoin, and Solana are not included due to limited label coverage and integration difficulty in the timeframe of this research. However, we were able to reliably source Solana data for Phantom, which is covered in a dedicated section below.

- The completeness of wallet coverage depends on available labels: some router addresses may be missing or outdated (e.g. older versions or unclassified deployments).

- This analysis does not capture swaps routed via external dApps, even if initiated by a wallet (e.g., a MetaMask user swapping directly on Uniswap)—nor does it include transfers between wallets.

- While not a complete picture, the resulting trendlines align closely with those from Dune Metrics' broader "Transfer Volume" charts (which looks at all net USD value transferred, not just embedded routers), suggesting the data is directionally robust.

Acknowledgements

We’re thankful to the many wallet teams and analysts who provided feedback, shared context, and helped refine both our dataset and methodology. This edition includes several new wallets thanks to teams that either engaged directly or had reliable onchain data available. If your project isn’t featured and you'd like to be included in future editions or research, please don’t hesitate to reach out.

Overall Trends in Swap Transfers and Volume

Swap activity via EOA wallets has shown strong long-term growth in terms of transfer count. From a peak of around 1 million weekly transfers during the 2021 bull market (November 2021), activity has surged to nearly 50 million transfers by the end of May 2025. This steady rise includes a sharp spike in April 2024, marking a key inflection point in onchain trading behavior.

Swap volume has followed a similarly cyclical and market-sensitive path. After hitting an all-time high of nearly $800 million in May 2021, volume surged again to nearly $1 billion in November 2021 before entering a prolonged bear market phase. Interestingly, by the time the FTX collapse occurred in November 2022, both volume and transfer activity had already fallen to local lows, suggesting that much of the market contraction preceded the event itself. For most of 2022 and 2023, volume hovered around $300 million weekly. A renewed wave of activity began in early 2024, with volume peaking at $1.5 billion in April. From November 2024 to March 2025, swap volume consistently remained above $1.5 billion per week, before dipping slightly. May 2025 has seen a new surge and marked a new all-time-high, showing signs of ongoing momentum heading into mid-year.

Swap Activity and Volume by Wallet Provider

The most prominent shift in EOA wallet activity over the past months is the explosive growth of Binance Wallet, which became the dominant source of both transfer count and swap volume starting in March 2025. Even after applying deduplication filters and refining our methodology, this trend remains significant and persistent.

By the last week of May, Binance Wallet swap volume reached an all-time weekly high of $27 billion, with over 44 million swaps executed. This surge dwarfs historical patterns and stands out even in a field of fast-growing wallets.

A couple of factors have been cited to explain this acceleration:

- Binance Alpha, a token discovery and pre-listing access program, initially launched in December 2024 and may have contributed to a longer-term baseline of activity. However, this does not fully explain the March–May spike: Alpha’s initial version was limited to Binance Wallet users, and the larger-scale rollout (Alpha 2.0) in May 2025 actually made the feature available to all Binance platform users, including those outside the wallet ecosystem. This likely had a greater impact on Binance Exchange activity than on wallet-level metrics.

- A more immediate and likely factor is Binance’s 0-fee swaps campaign, which began on March 17, and offers zero trading fees for swaps executed through the Swap, Bridge, and Quick Buy features in the wallet (excluding third-party dApps). This initiative directly incentivizes in-wallet activity and aligns more precisely with the observed growth pattern.

OKX, Bitget, Coinbase, and Rabby

While Binance dominates recent growth, OKX Wallet remains the second-largest driver of in-wallet swaps and volumes across chains. Despite a temporary decline in activity around March, due to OKX suspending its swap aggregator for security reasons, the wallet has rebounded strongly in May.

Bitget Wallet, which saw a dramatic rise in Q2 2024, had then entered a quieter phase, but has seen a new growth in activity levels in recent months. Meanwhile, Coinbase Wallet and Rabby, whose swap activity is inferred through fee collection, are notable beneficiaries of the improved data infrastructure in this version of the report.

MetaMask

Since emerging as the default EOA wallet in the 2021 cycle, MetaMask has remained a foundational player in the wallet landscape. While recent years have seen the rise of new competitors, MetaMask still commands a 15–20% share of transfers and volume, maintaining its relevance through a combination of ubiquity, extensibility, and continuous innovation. Rather than remaining a pure EOA product, MetaMask has gradually evolved into a broader wallet platform, spanning multiple layers of the stack:

- MetaMask Portfolio for multi-chain asset management

- MetaMask Snaps to enable custom plugin-like features

In the latest move in this direction, on June 2 2025 Consensys announced the acquisition of Web3Auth, a leading provider of embedded wallet infrastructure and social authentication. With this move, MetaMask integrates Web3Auth’s multi-factor auth and social login stack, allowing users to create and recover wallets with familiar methods like email and device-based authentication, and removing the seed phrase hurdle for the next wave of users.

For developers, the acquisition unlocks embedded wallet SDKs, account abstraction tools, and tighter integration with MetaMask’s infrastructure stack, including Infura and the Delegation Toolkit. Together, these changes support a hybrid wallet model: retaining EOA compatibility while gradually integrating programmable and abstracted wallet logic beneath the surface.

This direction mirrors a broader theme throughout the report: wallets are no longer just keys and interfaces. They are programmable infrastructure, increasingly modular, and deeply integrated across chains and app layers. MetaMask’s evolution reflects this shift, from browser extension to full-stack platform, from seed phrase to social login, from EOA to abstracted execution.

Chain-Level Dynamics

The Binance Wallet boom has also reshaped the chain distribution of swap and transfer activity and BNB Chain unsurprisingly mirrors this rise, currently leading in total transfers and swaps. Filtering out BNB reveals a more nuanced picture:

- Ethereum still leads by volume, accounting for nearly 70% of non-BNB swap value.

- Base has emerged as the leader in transfer count, reflecting its growing role as a low-cost environment for wallet-native activity.

- Polygon, Arbitrum, and other Layer 2 networks continue to contribute meaningfully across both metrics, reflecting the broader trend toward multichain distribution.

Key Takeaways

- Wallets are becoming primary swap venues: The steady growth in weekly swap count confirms that wallets are no longer just onboarding gateways but core venues for token trading, driven by convenience and integrated UX.

- Adoption grows faster than capital: While swap count has steadily increased, volume has fluctuated more across cycles and has grown less. This suggests a broader, more active user base but smaller average trade sizes, pointing to retail adoption and utility-led growth.

- Market maturity: While market share has shifted significantly from MetaMask’s early dominance, all major wallets analyzed have grown in absolute terms. The result is a more diverse ecosystem, shaped by differing strategies across regions, user types, and design philosophies.

- Binance dominates recent growth: Binance Wallet surged to 44M weekly swaps and $27B in volume, leading with over 90% of swaps and volume at peak. Almost identical shares are recorded for BNB Chain, showing the powerful flywheel between wallet and native chain, a model Coinbase and Base are optimizing as well.

- Ethereum remains the value layer: Ethereum’s swap share fell to about 10% but still accounts for 40% of volume, leading high-value trades. Meanwhile, BNB and Base now drive the majority of embedded swap activity, reflecting their traction for high-throughput, cost-efficient transactions.

Phantom Wallet: Solana’s Powerhouse

Dashboard: Phantom wallet

Data credits: Phantom team

Phantom is the only wallet we were able to track and confirm for Solana-based embedded swap activity. We analyzed both swap count and volume by identifying Solana addresses collecting Phantom’s in-app swapper fees, and reverse-engineering total traded volume and estimate weekly swap counts.

Phantom Wallet has long been the leading self-custodial wallet in the Solana ecosystem, and since 2022 it also expanded to selected EVMs. With its embedded Swapper feature launched in June 2021 and significant upgrades in 2023 and 2024, Phantom has increasingly become a powerful trading hub, particularly for Solana-native users. Recent new features like SOL staking and social features make Phantom a full-fledged platform.

In November 2023, Phantom introduced the Cross-Chain Swapper, a bridging interface integrated directly into the Phantom UI, which allows users to bridge tokens across Ethereum, Polygon, Base, and Solana without leaving the wallet.

In November 2024, Phantom integrated the OKX DEX API to power its in-wallet Solana swaps. This upgrade enabled Phantom to route trades across more than 400 DEXs and 18 cross-chain bridges, optimizing for best price, low slippage, and minimal latency.

Explosive Growth in Embedded Swap Activity

Since November 2024, Phantom has experienced a dramatic surge in embedded swap activity:

- Swap count peaked at 10 million weekly in late November, before stabilizing at around 3.4 million by May 2025.

- Swap volume hit an all-time high of $5.7 billion in January 2025 driven by the peak of the memecoin frenzy, then settled to a steady $700-$800 million per week.

At its height, Phantom embedded swaps alone accounted for over 10% of total Solana transfer volume in the week of January 20 2025 ($53B), and reached 20% share during several weeks in November and December 2024.

Interestingly, the January surge also triggered a temporary spike in Ethereum swaps, with Phantom processing $500 million in a single week, up from a typical baseline of ~$20 million—likely a result of users bridging assets into Solana amid heightened market activity.

This growth is overwhelmingly Solana-driven, with 97% of swap activity and volume occurring on the chain—firmly establishing Phantom as the leading wallet for the Solana ecosystem.

🅽🅴🆆

Phantom’s overall trajectory exemplifies one of the central themes of this report: the convergence between wallets and applications. What began as a streamlined self-custody wallet for Solana is increasingly positioning itself as a full-featured, vertically integrated DeFi and social platform.

The recent launch of PSOL, Phantom’s native liquid staking token, is a prime example. In under two weeks, PSOL has surpassed $15M in market cap with over 17K holders, signaling early traction.

DEX data reflects active retail participation: nearly 700 trades, $7.3M+ in volume, and an average trade size of $790. Notably, while Orca holds a sizable $1.8M stake (12.8% of supply), over 58% of PSOL is held by addresses with less than 0.5% of supply—indicating broad distribution. By issuing its own LST, Phantom is no longer just facilitating DeFi access—it’s embedding deeper into Solana’s staking and liquidity layers, expanding its role in the ecosystem’s financial infrastructure.

At the same time, Phantom is reimagining wallet UX around onchain social discovery. Its new feed feature, now in beta, surfaces real-time onchain activity. Users can follow, react, and curate their experience by tracking wallets and tokens directly within the app. Combined with tools like customizable privacy controls and token-based notification streams, this marks a shift from transactional interface to social platform.

Together, these moves highlight how Phantom is evolving from a gateway into Solana to a full-stack crypto application in its own right, handling staking, swapping, social interactions, and portfolio curation under one roof.

Key Takeaways

- Solana-Native, Cross-Chain Capable: While Phantom now supports Ethereum, Polygon, and Base, 97% of its embedded swap activity and volume occur on Solana, confirming its position as the leading self-custodial wallet in that ecosystem.

- Massive Onchain Footprint: Swap count peaked at 10 million weekly, with volume hitting $5.7 billion in January 2025. At its peak, Phantom embedded swaps accounted for over 10% of all Solana transfer volume, reaching up to 20% during several weeks in late 2024.

- Expanding Into Platform Territory: With features like in-app staking and PSOL (its native LST) and social feeds, Phantom is evolving into a vertically integrated DeFi and social hub. Not just a wallet, but a full-stack application driving liquidity and discovery on Solana and beyond.

🅽🅴🆆 Uniswap Wallet: From Interface to Execution Layer

Dashboard: Uniswap X

Dashboard: Uniswap X: Orders filled

Most wallets began by managing keys, then gradually layered on swap features. Uniswap Wallet inverts that path: it extends from one of crypto’s most successful DEXs into wallet infrastructure. This origin story defines its architecture. Rather than embedding a swap router into a generic wallet, Uniswap Wallet is built around the Uniswap Trading API, which integrates Uniswap v2, v3, v4 and UniswapX, its native intent-based protocol that enables modular, gasless, MEV-resistant trading.

Launched in 2023, UniswapX introduced a new paradigm: users sign off-chain Dutch auction-style orders ("intents"), which are then competed over and filled by third-party fillers on-chain. The result is improved pricing, zero gas or revert costs for users, and enhanced resistance to frontrunning, without compromising liquidity access.

Activity Trends

Usage metrics from the UniswapX ecosystem reveal a clear distinction between demand and supply dynamics.

On the demand side, activity has followed a more cyclical pattern. Weekly filled orders surged during key periods in June 2024, January 2025, and again in May 2025, followed by intermittent slowdowns. Despite this volatility, weekly orders have consistently remained above 40,000 in May.

The number of unique swappers shows a similar pattern: peaking at 22,000 in December 2024, dipping through Q1 2025, and recently rebounding to over 15,000 weekly users.

By contrast, unique fillers, the agents that execute trades, have grown steadily and consistently, reaching an all-time high of 73 in February 2025 and consistently above 60 throughout May.

This divergence suggests a healthy maturation of the filler ecosystem, with increasing supply-side participation regardless of short-term shifts in user activity and demand.

Overall Ethereum, the first chain to support UniswapX, led early adoption, but Base has since overtaken it in terms of volume. Meanwhile, Arbitrum stands out for its high share of unique fillers, even with a smaller slice of total swap volume.

According to Flashbots, total swap volume via UniswapX (on Ethereum only) has surpassed $21B. Interestingly, while order count peaked in early January 2025, volume dipped during that same week, likely a sign of many smaller retail users entering the protocol.

On Ethereum, the share of swaps routed through UniswapX has steadily grown and now accounts for approximately 30% of all Uniswap swaps. Most other chains still rely primarily on the Universal Router.

Introducing Smart Wallets: A UX Leap

Uniswap is now preparing to take its wallet evolution one step further by releasing its Smart Wallet, built to fully embrace account abstraction and optimize transaction flow. This includes support for both EIP-7702 (temporary delegation) and ERC-4337, positioning Uniswap Wallet as a programmable smart account hub.

Key features include:

- Seamless delegation via EIP-7702 to Uniswap’s own smart wallet contract

- Support for ERC-5792, enabling batched transactions such as approve + swap in a single click.

- Future plans for additional batching (e.g. approve + LP, or bridge + swap).

- ERC-4337 compatibility, paving the way for gas sponsorship and ERC-20 gas payments.

- Native support for passkeys and session keys, allowing users to authorize new signers and unlock more complex trading flows.

All newly created wallets in the Uniswap Mobile app and browser extension will adopt the smart wallet by default. Legacy EOAs can opt in via delegation. By focusing on delegation and modularity, Uniswap aims to offer a seamless user experience without requiring full wallet migration, a hybrid approach that reflects the broader shift across the wallet landscape.

A Wallet Optimized for Coordination, Not Just Access

Uniswap Wallet sits at the intersection of several powerful trends reshaping wallet user experience. First, its native integration with the Uniswap protocol and UniswapX gives it unparalleled access to deep liquidity, both on-chain and off-chain, through a competitive network of fillers and auction engines. Second, intent-based execution via UniswapX positions the wallet to benefit from a broader shift toward abstracted user flows, where swaps and other onchain actions are coordinated, not manually signed step-by-step. Third, the upcoming release of Uniswap’s smart wallet introduces critical account abstraction features, such as batched transactions, delegated signers, gas sponsorship, and passkey support, all designed to make advanced onchain activity feel seamless. These combined tailwinds make Uniswap Wallet more than just an access point to a DEX; they establish it as a programmable coordination layer poised to redefine what a wallet can do.

Key Takeaways

- DEX-Native Advantage: Uniswap Wallet flips the traditional wallet model by building from a leading DEX outward, integrating deeply with UniswapX to offer users gasless, MEV-resistant swaps across on-chain and off-chain liquidity sources through intent-based execution.

- Smart Account Ready: With the upcoming Smart Wallet rollout, Uniswap is blending EOA familiarity with smart wallet flexibility, unlocking batched transactions, gas sponsorship, delegated signers, and passkey support, all designed to streamline complex trading into a seamless user experience.

🅽🅴🆆 Meteor Wallet: A Multichain Window into NEAR

Dashboard: Analytics

Meteor Wallet stands out as a leading interface for the NEAR ecosystem, while also offering robust multichain support. With the rollout of Meteor V2 and the launch of its mobile app beta in early 2025, the wallet is evolving into a faster, more unified experience across platforms.

Like several wallets featured in this report, Meteor offers a rich set of DeFi-native features, including a built-in swap interface and seamless dApp access via its in-wallet browser. Meteor also leverages unique capabilities of the NEAR blockchain, such as intent-based execution, which now powers 100% of its cross-chain bridging.

Over the past 90 days, Meteor averaged 25K daily active wallets and 45K daily transactions, with activity covering both swapping and bridging.

Swap volume fluctuated significantly day-to-day, ranging from ~$20K to over $150K, with a weekly average above $200K.

Swaps are dominated by pairs involving USDC, NEAR, and USDT, with NEAR and USDC consistently appearing as the most common “to” tokens. The top pairs are:

- USDC → NEAR with $600k in the past 90 days

- NEAR → USDC with $338k.

This reflects both the liquidity structure of the Near ecosystem and user behavior centered on local currency conversions. Meteor’s integration with NEAR-native tokens (e.g., wrap.near, meta-pool.near, usdt.tether-token.near) further shows its alignment with local DeFi protocols, rather than serving as a generalized multi-chain swap tool.

Cross-Chain Bridging: Near as a Hub

Bridge activity saw an average of ~$50K weekly, with occasional spikes tied to specific chain flows.

Bridge data over the past 90 days shows 77% of bridge activity originates from Near, with the rest primarily from Solana (14%) and Arbitrum (7%). On the receiving side, Solana dominates at 40%, followed by Near (24%), Ethereum (23%), and Arbitrum (9%).

The top bridge flows by token volume include:

- NEAR → SOL: $395K

- NEAR → ETH: $231K

- SOL → NEAR: $143K

These patterns position Meteor as a key liquidity hub between NEAR and other chains (especially Solana) and highlight the growing role of wallets as active coordinators of cross-chain value flow. By natively leveraging NEAR’s intent-based architecture, Meteor can offer a smoother, more programmable multichain experience, with abstracted gas fees and seamless bridging logic. This approach shows how deeply integrated wallet design, aligned with the capabilities of the underlying chain, can unlock more powerful user experiences and make multichain activity feel native.

Key Takeaways

- Chain-Native Advantage: By fully leveraging NEAR’s intent-based architecture, Meteor enables seamless, gas-abstracted swaps and bridging, positioning itself as a programmable liquidity hub for multichain coordination, especially between NEAR and Solana.

- Ecosystem-Embedded Design: Rather than acting as a generic multichain wallet, Meteor is tightly integrated with NEAR-native protocols and tokens, aligning its UX and liquidity flows with the unique structure of the NEAR ecosystem.

Ronin Wallet: A Purpose-Built EOA Wallet

Dashboard: Ronin EOA Wallet

Data credits: Ronin team

Ronin Wallet was originally developed to serve the Ronin ecosystem—a gaming-centric blockchain spun out of Axie Infinity—with features and onboarding flows tailored to the specific needs of both gamers and game developers. It prioritized accessibility and simplicity, offering:

- Social login onboarding (e.g. email, Google), avoiding traditional seed phrase friction

- In-wallet fiat onramps, supporting payments via card, Apple Pay, and Google Pay

- Batch NFT transfers for gaming assets

- In-wallet game discovery, including an ecosystem calendar

- Developer tools for seamless wallet provisioning and quest-based user engagement

These design choices paid off: active user numbers have remained remarkably stable, averaging around 400,000 weekly users since 2023, with spikes above 600,000. Importantly, all this activity has taken place within the Ronin ecosystem, including dApps, games, and assets native to the chain.

Ronin's in-wallet swap feature has seen much faster growth:

- Weekly swap count peaked at 270,000 in January, before stabilizing around 40,000.

- Swap volume topped $55 million weekly in early 2025, with a current YTD average of $20 million.

These metrics exclude external DEX interfaces or bridging tools used by Ronin wallet users.

The two recent spikes in activity highlight Ronin’s responsiveness to ecosystem catalysts:

- November–December 2024 saw a notable uptick in onchain activity, likely linked to broader market optimism around election season.

- In January 2025, activity surged again—this time tied to the launch of Tama.meme, Ronin’s own take on the “pump.fun” meme coin meta. The wave of meme coin speculation led to a surge in wallet interactions, swaps, and user onboarding.

While these figures trail larger general-purpose wallets with multichain reach (e.g. MetaMask or Phantom), they are significant in the context of a single-ecosystem wallet primarily used on Ronin.

Toward a Broader Ecosystem

With the launch of Open Ronin, the wallet is broadening its scope beyond gaming into consumer and DeFi applications. Recent updates have expanded chain support to include Base, Arbitrum, Polygon, BNB Chain, and Ethereum. While most of the advanced functionality remains centered on the Ronin chain for now, upcoming releases aim to extend full feature parity across these networks.

In many ways, Ronin represents a different kind of entry point into Web3—one rooted in entertainment-first use cases but now moving toward broader composability. As its ecosystem grows beyond games, Ronin will be a key player to watch in shaping how user experience and distribution evolve for crypto apps beyond finance.

Key Takeaways

- Designed for gamers, Ronin Wallet has sustained ~400K weekly users with spikes tied to ecosystem events like Tama.meme. All activity remains native to the Ronin chain, showcasing the power of a laser-focused approach: optimize for one niche, and keep shipping.

- After consolidating its core user base and use cases, Open Ronin is an ambitious attempt to export that success across chains—bringing its streamlined UX and embedded tools to ecosystems like Base, Arbitrum, and BNB Chain.

Addressable: Regional Wallet Usage

Dashboard: Regional Usage

Data credits: Addressable

This section explores the global footprint of crypto wallets by analyzing their user base (Total Users) and capital distribution (Balance) across geographies. The analysis highlights how wallet adoption varies across regions due to regulation, infrastructure, and product positioning.

The data is powered by Addressable, a Web3 growth platform that links on-chain wallet addresses to off-chain identifiers such as social profiles, mobile behavior, and browser metadata. This linkage enables a user-centric perspective on blockchain activity—moving beyond address-level analysis to more accurately represent real users.

The dataset consists of a random sample of 15 million users, filtered to include only countries and wallet providers with over 15,000 users. Each user is assigned a primary country via internal heuristics and de-noised to minimize the impact of VPNs, spoofed IPs, and low-confidence geolocation signals. While some bias remains, the sample is directionally accurate and statistically significant, representing a meaningful share of the estimated 30–60 million monthly active crypto users identified by a16z's State of Crypto 2024.

The analysis draws on EVM wallet addresses (Ethereum, BNB Chain, Polygon, Arbitrum, Avalanche, Base, and Optimism). Non-EVM wallets (e.g., Solana, Bitcoin) are included where possible by associating them with known EVM addresses, but some underrepresentation is expected. Only self-custodial wallets are covered in this analysis.

Regional Insights by Wallet Provider

All charts in this section come from this query.

OKX

OKX shows strong regional dominance in Asia, with user concentration highest in Singapore (13%), Vietnam (9%), and Hong Kong (8%), followed by Indonesia, Japan, the Philippines, and India. Nigeria (7%) and the US (4%) also have meaningful user shares. However, capital is concentrated elsewhere—particularly the US, which accounts for nearly 50% of wallet balance, with France (12%) and Indonesia (11%) following. Vietnam, despite high user count, represents only 0.1% of funds held. In 2024, transaction count was broadly distributed: US (8%), Japan and Indonesia (7%), and several East Asian and European countries contributing ~3–5%.

Bitget

Bitget’s user base is even more Asia-centric, led by Bangladesh (22%), Indonesia (15%), and India (9%). Nigeria (19%) is a unique outlier, the only non-Asian country in the top five, indicating Bitget’s grassroots success in key emerging markets. Capital, however, is highly concentrated in wealthier Asian nations—South Korea leads with 56%, followed by China (18%) and the UAE (15%), despite collectively contributing less than 2% of users. Transactions were concentrated in the US (43%), with Indonesia (14%) and Japan, Bangladesh, and India following at lower single-digit percentages.

Coinbase

Coinbase retains its North American and European focus. The US leads in user share (37%), followed by Germany, the UK, France, and Canada. South America contributes modestly, with Brazil at 2%. Interestingly, most wallet balance is held by Canadian users (58%), followed by the UK (18%) and US (16%). For transactions in 2024, the US accounted for 35%, with France, Germany, and the UK each near 4–6%. While user counts suggest global reach, balance data underscores Coinbase’s positioning as a capital-heavy custodian for Western users.

MetaMask

MetaMask continues to be the default non-custodial gateway, especially in emerging markets. Nigeria leads user share (12%), followed by Indonesia, India, the US, and Germany. However, balance distribution skews heavily toward developed markets: the US (12%), South Korea (7%), France (5%), and Portugal (4%) dominate. Nigeria’s balance contribution is minimal at 0.1%, reinforcing its role as an onboarding tool rather than capital store. Transactions were global: US and Taiwan (8%), Hong Kong (6%), and Japan (5%), showing widespread activity.

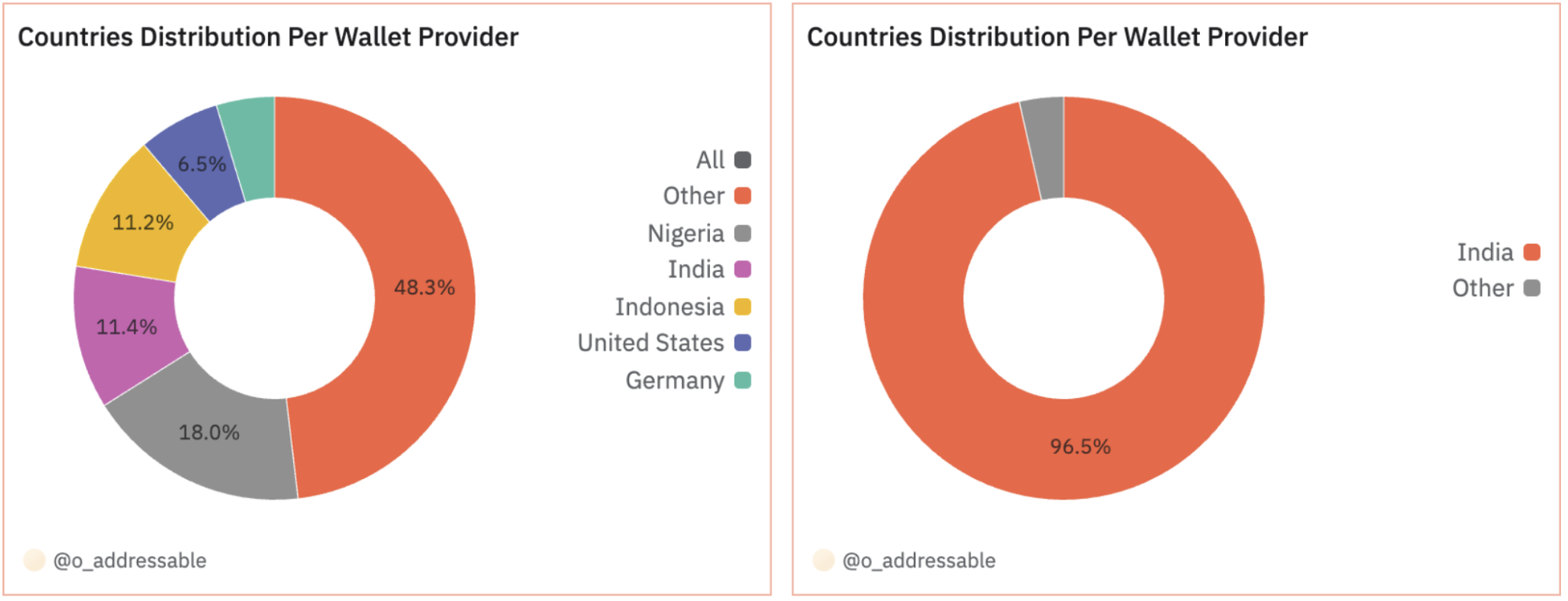

Phantom

Phantom displays a similar pattern to MetaMask in adoption-versus-capital. Nigeria (17%), India (11%), and Indonesia (10%) lead for users, but 96% of wallet balance is concentrated in India—suggesting a few large users perhaps originally from the Solana ecosystem. The US and Mexico follow, but with much smaller capital shares. For transactions, the US dominates with over 90%, likely reflecting both power users and strong Solana engagement.

Rabby

Rabby presents a more balanced picture across geographies and metrics. Nigeria (13%) and India (9%) lead for users (on the left), followed by France, Germany, and the US. On the capital side (Balance, on the right), France (12%), Germany (9%), and North America (US and Canada, 8% each) are dominant. Nigeria’s capital share remains low (0.16%), indicating the same usage/capital divergence seen in other wallets. Transaction data highlights France (14%), US and Indonesia (8%), Spain (7%), and India (6%) as leading activity hubs.

Most Popular Wallets by Country

All charts in this section come from this query.

Across regions, MetaMask remains the most widely used wallet, often leading both in user count and total balance. However, local variations reveal how regional ecosystems and preferences shape wallet adoption.

United States: MetaMask leads with 60% of users, followed by OKX (15%) and Trust (12%). In terms of capital, it's a two-player race: OKX (47%) and MetaMask (42%) hold nearly all user balances—suggesting MetaMask’s broad appeal and OKX’s concentration among high-value users.

China and South Korea:

- In China, MetaMask controls 87% of users and 61% of funds, but OKX (20%) and Bitget (15%) play a larger role in balance share than user count suggests.

- South Korea sees MetaMask (68%) and OKX (25%) lead on users, but Trust and Bitget also register notable balance shares.

Southeast Asia:

- In Singapore, users split between OKX (60%) and MetaMask (35%), while MetaMask slightly edges OKX in balance share (53% vs. 45%).

- Indonesia shows a similar pattern: MetaMask leads with 59% of users and 57% of balances, with OKX close behind (23% users, 41% balance).

India and Nigeria:

- In India, MetaMask dominates across the board: 63% of users and 79% of funds, with Phantom surprisingly holding 17% of balances despite low user share.

- Nigeria also favors MetaMask heavily—71% of users and 75% of funds—followed distantly by OKX and Bitget.

Europe:

- Germany: MetaMask leads with 70% of users, but Trust Wallet surprisingly holds 57% of the country’s wallet balances—signaling a strong trust in its storage capabilities.

- France: MetaMask commands 76% of users, but OKX captures a notable 38% of capital—suggesting it appeals to fewer but higher-balance users.

Latin America:

- In Brazil, MetaMask holds 71% of users, but Trust Wallet surprisingly holds 74% of total balances, hinting at regional capital trust preferences.

- Argentina shows an unusual split: users are evenly divided between MetaMask (50%) and OKX (43%), but 96% of balances sit with MetaMask, pointing to deeper financial usage.

Key Takeaways

- Some wallets like OKX and Bitget show strong regional clustering, particularly in Asia. Coinbase dominates in North America and parts of Europe. Others (MetaMask, Phantom, Rabby) have a more globally distributed user base, with usage common across emerging markets and capital concentration in developed ones.

- Switching from user count to wallet balance dramatically shifts the map. Capital is more concentrated in developed markets, regardless of the number of users.

- Emerging markets drive adoption, developed markets bring liquidity. For teams and protocols, this split may influence both growth strategy and monetization focus.

- MetaMask and OKX are the most common wallets across most major countries for both usage and funds held.

Section 02 - Smart Wallet Accounts

The Rise of Smart Accounts

What Are Smart Accounts and Why They Matter

Smart account wallets—also known as smart contract wallets—are programmable accounts controlled by smart contracts instead of by a private key, like EOA wallets. This architectural shift unlocks a range of features like:

- Account recovery without a seed phrase, using trusted entities or "guardians" (known as social recovery) to help restore access if keys are lost

- Multi-signature access control baked into the wallet logic

- Gasless transactions via relayers and paymasters

- Bundling and batching of multiple actions into one transaction

- Modular upgrades with customizable permissions and extensions

A core enabler of this shift is ERC-4337, the Ethereum standard for account abstraction. Rather than requiring changes to Ethereum’s consensus layer, ERC-4337 introduces a higher-layer system centered around a contract called the EntryPoint.

Under this design, users submit UserOperation objects—a type of pseudo-transaction that encapsulates the user’s intent, signature, nonce, gas constraints, and more. These are collected in a separate UserOperation mempool, distinct from Ethereum’s transaction mempool. Bundlers, which can also be validators, listen to this mempool. They validate and package UserOperations into a single transaction, which they send to the EntryPoint contract. The EntryPoint then verifies and executes these operations on behalf of the users’ smart accounts. Optionally, Paymaster contract can sponsor user gas fees or enable payments in ERC-20s.

This architecture standardizes how smart wallets interact with the chain while giving wallet developers flexibility to innovate on user experience and security. Notably, the paymaster mechanism allows gas to be paid in tokens like USDC or sponsored by third parties—unlocking much more user-friendly onboarding.

Importantly, not all smart accounts are necessarily compatible or use ERC-4337. While ERC-4337 is the most common standard for account abstraction, some wallets, like Safe and Argent, don't currently use ERC-4337. Safe has adopted a modular and flexible approach to integrating the ERC-4337, allowing users to turn their Safe account into an ERC-4337 smart account via a dedicated module.

ERC-4337 Smart Wallet Accounts

This section explores the evolution of smart wallet adoption through two key indicators: account deployments and UserOperations (UserOps)—the core transaction mechanism enabled by ERC-4337. The dataset only covers ERC-4337 compatible smart accounts, so the count may be lower than the actual number (Safe and Argent also use non-ERC4337 standards so they may be underrepresented).

Account Deployments

Smart account creation saw explosive growth in mid-2024, reaching a peak of over 1 million deployments in a single week in July. Since then, activity has cooled, with current levels hovering around 120,000 weekly deployments—about one-tenth of the July peak.

Since the introduction of account abstraction in early 2023, Polygon has consistently led in account deployments. However, its dominance has shifted:

- Base began rapidly gaining ground in July 2024 and now accounts for over 65% of weekly deployments.

- Arbitrum also experienced a notable spike in March 2025, briefly reaching 60% of deployments.

Focusing on smart account factories identified in labels.contracts (i.e., known named deployments), we observe strong competition among major providers:

- Biconomy was the dominant factory throughout most of 2023.

- (Gnosis) Safe began steadily increasing its share in early 2024 and currently leads in deployment volume.

- Zerodev surged to the top position briefly in October 2024.

- Stackup recorded two distinct peaks: July 2024 and March 2025.

- Coinbase emerged as a significant factory in 2025, consistently ranking among the top 5 and showing continued growth.

This diversification reflects the growing maturity and fragmentation of the smart account ecosystem, as more providers and wallet frontends enter the space. It’s worth noting that this methodology captures only labeled factory contracts, meaning the absolute number of account deployments in this breakdown is lower than the total by chain, and some market share estimates may be incomplete.

UserOperations

While account deployment has declined from its summer 2024 highs, overall UserOperations have continued to grow, rising from ~800,000 weekly ops in April 2023 to over 4 million by April 2025. The all-time high came in July 2024, with more than 5 million UserOps in a single week.

Although Polygon led in the early stages of account abstraction, Base has since taken over, particularly from mid-2024 onward:

- In the second half of April 2025, Base processed over 3 million UserOps per week, representing 87% of total weekly operations.

- Polygon held over 90% market share until April 2024, decreasing to 60% by July as Base gained traction.

- Arbitrum remains strong in third place, with intermittent surges in Q4 2024 and March 2025.

Bundling Trends

Interestingly, while the number of UserOps declined after the July 2024 peak, the number of bundles submitted to the EntryPoint contract has steadily increased. This suggests a broader growth in bundler diversity and competition, leading to smaller, more frequent bundles, likely a sign of healthier infrastructure and increased decentralization.

Key Takeaways

- Polygon led the initial wave of smart wallet deployments in 2023, but Base now dominates, accounting for over 65% of new deployments and up to 87% of weekly UserOperations in April 2025.

- Account deployments peaked in July 2024 with over 1 million in a single week, but have since declined to ~120K weekly, suggesting early saturation or a shift toward more targeted onboarding.

- UserOperations continue to grow overall, despite fewer new account creations. This indicates increased usage of existing smart wallets and deeper integration into DeFi and apps.

- Bundler activity is rising, as bundles per UserOp decrease, pointing to a maturing infrastructure and a more competitive bundler landscape.

- Factory-level dynamics are highly competitive: Biconomy led for much of 2023, while Safe gained traction in 2024. Zerodev briefly took the lead in October, and Coinbase has steadily climbed in 2025.

- Factory breakdowns are limited to labeled contracts, meaning some activity is undercounted.

- Growth patterns correlate with ecosystem strategy. Base’s rise, for example, mirrors active ecosystem investment and strong support for AA infrastructure by players like Coinbase.

🅽🅴🆆 Biconomy: A Case Study in Smart Account Modularity

Dashboard: Biconomy Smart Account Dashboard

Biconomy offers one of the clearest windows into the evolving smart account landscape. With over 1.9 million smart accounts deployed across multiple versions, it represents one of the most active and diverse factories in the ecosystem. The data, from deployment volumes and active accounts to chain-specific adoption and total value processed, offers valuable insight into broader themes discussed throughout this report: modularity, use case specialization, and additionally the challenge of selecting the best metrics to capture meaningful usage.

Account Deployment

Biconomy’s account deployment spans three major versions:

- V1 (non modular account): 762,000+ accounts (largely dormant)

- V2 (modular account): 890,000+ accounts (active across multiple chains)

- Nexus (modular account with native orchestration): 244,000+ accounts (launched in April 2025)

The launch of Nexus marked a new phase of adoption. In May 2025 alone, over 155,000 Nexus accounts were deployed, driven by integrations with apps like Mocaverse and Magic Newton.

While Polygon accounts for the majority of smart accounts overall, most of the recent accounts were deployed on Base, with Polygon ranking second, consistent with broader trends showing Base as an emerging leader in smart account adoption.

UserOps and Active Accounts: Usage Diverges by Version and Chain

Alongside deployment growth, active accounts now exceed 715K, with a 41% activity ratio across all deployed accounts. May saw a notable increase, mostly driven by Nexus (47K out of 63K), indicating strong early engagement with the newest account architecture.

Most active users were on Base, which counted 49K active accounts, followed by Polygon with 11K.

UserOps also rose in May, offering another lens into actual account activity. Interestingly, while Nexus led in new deployments and active accounts, V2 accounts generated the majority of May's UserOps with 300K out of 352K total, suggesting continued usage from existing integrations.

In terms of chains, Polygon led with 180K UserOps in May, followed by Base with 94K, reflecting how usage is distributed differently from deployment and active accounts figures.

Measuring Activity: TVL vs TVP

Whilst account deployments and UserOps were traditionally the original metrics to determine account usage, Biconomy’s recent focus on Orchestration has helped discover additional metrics. Orchestration enables developers to create multi transaction flows which are permitted by a single click. This changes the model of interacting with blockchains from one where users approve low level function calls to one where users approve the actions they want to achieve. As for metrics, Biconomy reports both TVL (Total Value Locked) and TVP (Total Value Processed), two distinct metrics that highlight different aspects of account usage:

- TVL captures the amount of capital held within smart accounts at a given time.

- TVP tracks the total value that has moved through accounts—i.e., how much has been used, swapped, bridged, or transacted.

Across all chains and account versions, by the end of May Biconomy had processed over $520 million in TVP. The vast majority of this activity comes from V2 accounts ($500M), with V1 accounts contributing $9M and Nexus already accounting for $8M+. The rapid growth of TVP occurred in 2025 due to use cases like orchestration and Defi, where smart accounts become a layer for a safer and cleaner UX through one-click experiences.

A closer look reveals striking variation by chain: Blast accounts alone account for over $360M in TVP, despite representing a small share of total deployments and holding negligible TVL. Other notable contributors include Polygon ($130M), Base with $14M and Arbitrum, which processed around $5M.

TVL, while lower in magnitude, offers insight into stored capital, with about $1M on Polygon, and ~$120K on Blast, out of a total TVL of $1.1M.

The Blast integration illustrates where TVP becomes the more relevant metric: users fund their Blast mobile wallets and immediately use those funds within the app, resulting in high value flow (TVP) but low TVL.

By contrast, in the case of Newton, the new wallet by Magic Labs, users may deposit funds and hold them for future activity. In these scenarios, TVL captures dormant capital, while TVP might understate engagement if transactions are infrequent or deferred via intent logic.

This variability illustrates why no single metric can fully capture smart account utility. TVL works well for custody-driven accounts but can understate active use in systems where throughput and transaction coordination are more relevant. TVP helps surface these flows but may overlook intent-based or delayed engagement. Given Nexus’ modular architecture with native orchestration, it serves use cases where TVL is important (e.g. wallets, embedded wallets) as well as the emergent use cases where TVP is important for apps and frontends that want to enable one-click flows, allowing the user to use any wallet of their choice.

Fragmentation, Modularity, and the Search for Better Metrics

Biconomy’s evolving architecture reflects broader protocol trends. Nexus is modular by design, fully compatible with ERC-4337, and built to support emerging features like intent-based execution and EIP-7702. It also forms the foundation for Biconomy’s revolutionary orchestration layer that introduces the Modular Execution Environment, a peer-to-peer system enabling cross-chain actions in a single signature. This shift points to a future where execution becomes abstracted from the wallet and dapp interface.

In the end, Biconomy’s data reveals a smart account ecosystem defined by versioning, chain diversity, and varying user behaviors. No single metric can capture this complexity alone. But together, they highlight a key transformation: wallets are no longer static tools for access; they're programmable coordination layers shaped by architecture, use case, and intent.

Key Takeaways

- Modular Evolution and Diverse Metrics: With over 1.9M smart accounts deployed across three architectures, Biconomy exemplifies how modular design, versioning, and orchestration reshape what usage looks like.

- Smart Accounts as UX Infrastructure: Nexus, Biconomy’s latest architecture, powers one-click, intent-driven flows across chains, revealing a shift from wallets as static storage to programmable execution layers that abstract complexity for users and developers alike.

Section 03 - Emerging Wallets Spotlight

Layer3 Wallet: Embedding Smart Accounts in a Consumer Crypto Platform

Dashboard: L3 Wallet

Data credits: Layer3 team

Layer3 is a consumer-facing crypto platform focused on discovery, onboarding, and user engagement through quests, token incentives, and app integrations. With millions of onchain actions processed through its interface, it has become a widely used entry point for both new and existing users to interact with dApps across networks. In April 2025, Layer3 introduced its own embedded smart wallet. Rather than serving as a general-purpose interface, the wallet is deeply integrated into the Layer3 app, enabling streamlined onboarding and interaction across Layer3’s core products while aligning infrastructure more tightly with its user journey.

The wallet uses a smart account architecture built on abstraction layers like ZeroDev Kernel, Pimlico, Turnkey and Dune Echo to power wallet balances and activity. Key features—such as passkey login, gas sponsorship, and chain abstraction—mirror broader smart wallet trends aimed at reducing friction for both crypto-native and new users. Importantly, the Layer3 wallet exists alongside support for external EOAs, allowing for flexible access and gradual migration.

Onchain Activity and Adoption Trends

Since launch, the wallet has generated 1.39 million UserOperations—a key activity metric for smart accounts—across 42,644 smart wallet deployments. The top five chains by number of deployed wallets are: Base (14K), Optimism (9K), Arbitrum (5K), Polygon (4.5K), and Mantle (2.2K). Notably, Base saw the fastest growth, doubling from 6K to 12K deployments in less than ten days in April.

While wallet creation peaked in March–April with daily highs of 1.6K, 3.3K, and 4.1K new accounts, the current pace has slowed.

However, UserOps have continued rising, growing from ~11K daily in March to over 30K in May—indicating deeper engagement among existing users.

Chain-level breakdowns show a clear early leadership of Base:

- Base accounts for ~66% of UserOps

- Optimism: ~20% of UserOps

- Arbitrum and Polygon: smaller but steady usage

- Newer chains like Ink and Berachain have also seen rising adoption

This divergence between new wallets deployment and ongoing usage suggests the wallet is becoming a stable interface for repeat interaction—rather than just an onboarding mechanism.

As smart wallets continue to blur the line between product and infrastructure, Layer3’s approach reflects one path forward: by embedding wallet logic directly within platform workflows, Layer3 can own more of the infrastructure stack and thus improve retention, reduce friction, and support more complex use cases natively.

Gem Wallet

Dashboard: Gem Wallet

“Gem Wallet is built in public where crypto is permissionless, multichain and open source so you can do more with your crypto.”

– Gem Wallet Team

Launched in 2023, Gem Wallet is a self-custodial, open-source and mobile-first wallet. With native support for Bitcoin, Ethereum, Solana, Base, Tron, Sui, XRP, and more, Gem has positioned itself as a flexible gateway to crypto for a global user base.

While the product shipped in 2023, Gem Wallet’s embedded swap functionality—the core focus of this analysis—went live in November 2024, following a brief dependency on third-party aggregators like 1inch. The launch of its own permissionless aggregator marked a key milestone, allowing Gem to progressively integrate protocols like PancakeSwap, Jupiter, and Thorchain without having to rely on third-party APIs. As each integration rolled out between late 2024 and early 2025, they contributed to visible bumps in both usage and revenue.

Swap Revenue and Activity Insights

- Since launching its own swap feature, Gem Wallet has generated over $81,000 in swap fees, with 2025 revenue already surpassing $73,000 as of late April.

- The bulk of fee revenue comes from Ethereum ($70K), followed by BNB Chain and a growing contribution from Arbitrum, particularly in Q2 2025.

- Most historical swap activity has been driven by BNB, although Ethereum has also been an important contributor, and more recently Base and Solana.

- On a protocol level, Thorchain stands out as the top revenue generator, with consistent activity also emerging across PancakeSwap and other newly integrated routes.

Adoption Curve and Forward Outlook

Given the late 2024 timing of its aggregator launch, weekly swap activity data is currently limited, but early signs point to healthy and growing engagement. The wallet has also seen incremental revenue bumps corresponding to each protocol integration—suggesting a product-led growth loop where expanded liquidity options directly drive increased usage.

As a relative newcomer, Gem Wallet’s swap data does not span the full reporting period covered in this analysis. Still, its recent metrics offer a glimpse into how quickly a lean, mobile-first wallet can capture value with the right infrastructure and timing.

Ambire wallet

Dashboard: Ambire Wallet

Ambire Wallet is a smart contract wallet built to streamline the self-custody experience while exposing users to the advanced capabilities of account abstraction. Designed with a user-friendly interface, Ambire introduces quality-of-life features such as:

- Human-readable transactions, reducing user error.

- Gas fee optimization, through transaction batching and stablecoin-denominated payments.

- A “gas tank” system for prepaying fees.

- Integrated swaps, fiat on/off-ramps, and broad network support (including Ethereum, Polygon, Base, Optimism, Arbitrum, Scroll, Avalanche, and Gnosis).

Adoption of Ambire Wallet accelerated significantly in early 2025. After a relatively modest baseline of ~50 transactions per day through much of 2024, activity surged in February, exceeding 1K daily transactions by May.

This growth appears tightly linked to the launch of Ambire Legends in December 2024, a gamified campaign designed to introduce users to the full spectrum of smart account features through a quest-based experience. Now transitioning into Ambire Rewards, the campaign combines educational missions with XP-based incentives and leaderboard mechanics. It encourages usage of features like gas sponsorship, account recovery options, transaction batching, and onchain governance, elements core to the future of wallet UX under account abstraction.

In terms of network distribution, historically, Ethereum accounted for the majority of Ambire Wallet activity (38%), followed by Polygon (24%) and BNB Chain (14%).

However, the recent Q1 2025 surge shifted this balance: Base became the leading execution layer for Ambire activity during this period, followed by Ethereum and Optimism, highlighting the wallet’s growing integration across the broader L2 ecosystem.

Ambire and EIP-7702

Ambire is among the first wallets to support EIP-7702, allowing EOAs to temporarily adopt smart account functionality without migrating wallets. By signing an onchain authorization, users can enable features like sponsorship and batching—revocable at any time.

As of May 2025, Ambire ranks among the top three identified delegates, with 32 active delegations, positioning it at the forefront of early 7702 adoption.

Key Takeaways

- Different architectures, different strengths: Ambire and Layer3 use smart accounts to enable features like gas sponsorship, session approvals, and passkey login. Gem—while not a smart account wallet—shows how lean, protocol-level integrations (e.g. Thorchain, PancakeSwap) can drive usage and fee capture.

- Incentives matter: Ambire’s XP-based rewards boosted feature exploration, while Layer3 benefits from launching its wallet inside an already active, incentivized ecosystem. Embedding a wallet within a platform that already drives user actions can create a powerful flywheel—accelerating smart wallet adoption from day one.

- Base: All three wallets show growing traction on Base, suggesting it’s becoming the default proving ground for new wallet products. Layer3 sees 66% of UserOps on Base, Ambire shifted activity there in Q1 2025, and Gem recorded a growing share of swaps on the chain.

- Execution styles vary, but user growth is visible: While Ambire leads in early adoption of new standards like EIP-7702, Layer3 optimizes flow within its app, and Gem targets modular liquidity access. These approaches illustrate how wallets are diversifying not just features—but also the ways they position themselves in the broader crypto UX stack.

Section 04 - Wallet Infra

Reown: Powering the Universal Wallets

Dashboard: Smart Accounts Dashboard

Data credit: Reown team

“The shift to smart accounts from EOA wallets reflects something bigger than a tech upgrade. It’s a signal that the infrastructure and user experience of wallets are finally converging. At Reown, we’ve created Universal Wallets leveraging Safe’s technology to meet that moment. Universal Wallets are secure and optimized for how users actually interact and build onchain. As we continue to move towards mainstream adoption, account abstraction and simplifying the process of being onchain is crucial for onboarding.”

– Jess Houlgrave, CEO of Reown

In 2024, Reown (the builders of the WalletConnect Network) integrated Smart Accounts as the default architecture behind its new Universal Wallets, part of the AppKit and WalletKit suite. This marked a shift from EOAs toward programmable wallets built on account abstraction. Rather than developing a proprietary stack, WalletConnect opted to embed Safe to improve security, onboarding, and interoperability across dApps.

This integration allows users to:

- Create and manage accounts through the Universal Wallet interface

- Benefit from modular security features like multi-sig and recovery modules

- Interact across wallets, dApps connected, or external protocols directly (e.g. Uniswap)

It’s also a strong signal of convergence between backend infrastructure (Safe) and frontend distribution (Reown AppKit), especially for onboarding retail and developer audiences into account abstraction.

Chain Distribution: A Shifting Landscape

Deployment patterns across blockchains reveal just how dynamic the smart account ecosystem has become:

- Optimism dominated early in 2024, peaking at nearly half of all deployments.

- Base quickly gained momentum during the summer and overtook Optimism by August, now accounting for 60%+ of new accounts, a clear sign of developer and app migration.

- Polygon experienced spikes in October, coinciding with a sharp rise in prediction market activity (notably Polymarket), and briefly led all chains with 45% of deployments.

- Ethereum has shown a steady rise in share since late 2024, reaching ~20% by April 2025—perhaps signaling growing demand for mainnet-grade security and permanence.

Active Accounts

The share of active smart accounts largely mirrors deployment trends, with Base dominating for most of the year—often holding between 30% and 55%. Notable deviations include:

- A sharp October uptick on Polygon, again possibly tied to US election-related usage.

- A gradual rise on Ethereum, with consistent growth pushing it to 15–20% share of active accounts by April 2025.

- Arbitrum has remained steady throughout, hovering just under 20%.

Transactions: Usage Lags for Some Chains

Transaction share adds a different layer of insight, showing where wallets are not just created—but actually used:

- Base has shown steady and sustained momentum, rising from 18% of smart wallet transactions in June 2024 to 43% by April 2025, establishing itself as a key execution layer for smart wallet activity.

- Optimism maintained a strong presence throughout 2024, reaching a peak of 55% in December.

- Polygon’s share varied across the period, with notable spikes, such as a jump from 3% in January to 38% in April, suggesting responsive adoption during key moments and campaigns.

- Arbitrum continues to play a solid role in wallet deployments and active usage, and its share of transactions remains around 10%, pointing to potential for future growth in execution volume.

- Ethereum is increasingly central for smart account deployment and active accounts, reflecting its foundational role. Its share of transaction execution also massively increased in May. Lower gas fees and more efficient execution thanks to various recent EIPs and the Pectra upgrade may further accelerate this trend.

Platform Usage: How Users Access the Wallet

Reown’s data also offers visibility into how users connect to smart wallets through AppKit. This connection method is more than a technical detail, shaping design decisions, integration strategies, and user experience.

- Browser-based connections have dominated throughout the year, consistently making up around 80% of sessions.

- Mobile wallets (including QR-based interactions) account for about 20%, with a 75/25 Android-to-iOS split.

This breakdown reflects the broader Web3 UX landscape: while mobile-first growth is accelerating globally, browser access remains the default for many dApp-heavy workflows. These insights are especially valuable for app developers as they prioritize which platforms and environments to support first.

Key Takeaways

- Universal Wallets Blend Access and Abstraction: By combining Safe’s smart account architecture with WalletConnect’s AppKit, Reown bridges the gap between advanced smart wallet capabilities and intuitive, app-agnostic user interfaces.

- Built for Mainstream-Ready UX: Reown’s focus on reusable sessions, cross-device continuity, and seamless smart account delegation reflects a broader shift toward wallets that feel like familiar login systems rather than crypto tooling.

Privy: Embedded Identity and Wallet Infrastructure

Dashboard: Privy

Data credits: Privy team

Privy has emerged as a foundational layer for onboarding and identity management in Web3, offering embedded wallets and authentication infrastructure for consumer-facing crypto apps. Rather than asking users to install wallets or manage keys, Privy enables products to create seamless onboarding flows where wallets are provisioned automatically at login—whether via email, social login, or passkey. Its infrastructure is built for performance at scale, with key user experience metrics that rival traditional fintech:

- Wallet creation speed: <200ms average time to provision a wallet after login

- Signature speed: <20ms average latency for executing wallet signatures

- Wallet activity: Over 183M embedded wallet signatures and 180M transactions processed year-to-date (YTD)

Privy wallets are typically provisioned when users login with one of Privy's supported authentication methods. This table breaks down wallet creation by login method (YTD):

- Email is still dominating with 40%

- Twitter (35%)

- Followed by Telegram (9%), Farcaster (6%), the only web3 method used.

Privy wallets are created when our customers' users sign up for their products. This table breaks down wallets provisioned based on customer product category (YTD).

- Social apps (53%)

- Followed by enterprise (17%), gaming (11%), fintech/trading (11%), and AI products (8%)

As onchain applications evolve toward smoother UX and composable onboarding, Privy plays a critical role in bridging Web2 familiarity with Web3 functionality—provisioning wallets that are ready for smart account features from day one.

Key Takeaways

- Frictionless Onboarding at Web2 Speeds: Privy enables wallet creation in under 200ms through familiar login methods like email (41% share), accelerating adoption without sacrificing self-custody.

- Ubiquity Across App Types: With 183M signatures YTD and top usage across social (53%), fintech, and consumer apps, Privy shows that embedded wallets are now foundational to a wide range of verticals.

🅽🅴🆆 Dynamic Wallet: Flexible Wallet Architecture for the Modular Era

Dashboard: dune.com/dynamic_xyz/wallets-report/25c9a8af-9aeb-4276-a0f5-92aa80cce96a

One of the clearest trends emerging from the wallet landscape is that developers are no longer building for a single wallet—they’re building for a wallet layer. Rather than choosing between embedded or external access, hybrid infrastructures are becoming the default. Embedded wallets streamline onboarding for new users, while EOAs remain vital for experienced users, interoperability, and cross-app continuity.

Dynamic reflects this shift by providing flexible and modular wallet infrastructure that prioritizes user-friendly onboarding. Specifically, it enables apps to support both embedded wallets and external EOAs through a single SDK, offering flexible, user-friendly onboarding across high-throughput chains like EVM and Solana.

Adoption data from apps using Dynamic highlights this dual-track trend: while EOA-based access remains foundational and these wallets represent most of the wallets connected via Dynamic, embedded wallets have been growing more than 3x faster than EOAs.

In early 2024, fewer than 1 in 5 apps on Dynamic provisioned embedded wallets. As of May 2025, that figure has doubled to 40%, signaling growing developer preference for seamless onboarding.

The balance between external EOAs and embedded wallets varies notably across ecosystems. On EVM, MetaMask maintains a dominant position, accounting for nearly 50% of wallet connections among apps using Dynamic. It’s followed by OKX and Dynamic’s embedded wallets, each with around 18% share, while Rabby holds a solid ~7%.

On Solana, Phantom leads with approximately 40% of usage, although embedded wallets are quickly catching up, now making up a full third of connections. Notably, Magic Eden Wallet has also emerged as a strong contender, capturing around 12% of the share.

Beyond user-facing wallets, Dynamic also supports emerging backend use cases, like developer-controlled wallets for stablecoin payouts, onchain agent flows, and treasury operations. As ecosystems like Sei explore unified “global wallets” that anchor identity across dApps, Dynamic illustrates how wallet infrastructure is evolving from frontend UX to programmable backend rails.

Overall, data from Dynamic reinforce a key point: wallet usage is fragmented and becoming more so. No single wallet dominates across chains, user types, or application categories. Developers are no longer building for "the wallet," but for a wallet layer, an abstraction that includes EOAs, embedded accounts, and even programmable server-side wallets used for automation, payouts, and onchain agents.

As the definition of “wallet” continues to expand, so too does its role. It’s not just a front-end anymore. Wallets are becoming composable infrastructure: modular by design, programmable by default, and deeply integrated into the app experience.

Key Takeaways

- Hybrid by Default: Dynamic empowers developers to support both EOAs and embedded wallets via one SDK—allowing seamless onboarding for new users and preserving flexibility for power users.

- Usage Reflects Fragmentation, Not Winner-Take-All: While EOAs like MetaMask and Phantom dominate by chain, embedded wallets are growing 3x faster—showing developers are building for a “wallet layer,” not a single winner.

Dune’s Vision for Wallet Data Empowerment

At Dune, we believe data is the backbone of innovation in web3. Our mission has always been to make crypto data accessible. With this report, we’ve showcased how wallet data isn’t just a tool for analytics—it’s the foundation for building smarter, more intuitive applications that empower users to own and navigate their digital lives.

Now, we’re taking that vision further.

Introducing Sim: Powering the Future of Onchain Apps

On May 20th, Dune launched Sim, a brand-new multichain developer platform designed to become the backend infrastructure for every wallet, portfolio tracker, and user-facing application in web3. Sim provides instant, structured access to the most critical wallet data, with six initial endpoints tailored for seamless integration:

Building a wallet?

Power your wallet app with sim.dune.com

We hope you enjoyed this report!

To continue improving this picture, we invite wallet providers, analysts, and researchers to reach out and share additional data, insights, and context. By working together, we can build the most accurate and nuanced map of wallet usage across crypto.

Data inquiries:

filippo@dune.com

Want to be featured in upcoming reports like these?

Email alsie@dune.com or TG @alsieliu

Get started on Dune:

dune.com

Get started on Sim:

sim.dune.com

The wallet data must flow.

Disclaimer

This report reflects the current views of Dune analysts and may not be updated as circumstances change. Past performance does not guarantee future outcomes, as market conditions, regulations, and methodologies evolve over time. The information is provided “as is” without warranty, and Dune, their affiliates, or contributors shall not be liable for any damages arising from its use. No graph, model, or analysis herein should be the sole basis for investment decisions. This report does not constitute an offer or solicitation to buy/sell, and investors should seek professional advice tailored to their needs.

Ready to bring your Blockchain to Dune?

Power your App with Dune data

Steam Dune data in your analytics environment

Want to join Dune?

.png)

Dune Datashare

Ready to get started?

Individuals + Small Teams

Enterprise